Part I made the autonomy case: a mortgage doesn't just take your money. It takes your options. This is the investment argument. Nineteen years of data, and what I choose instead.

I know people who got rich from real estate. Real people. Not hypotheticals.

I know a couple who started building a portfolio alongside their day jobs. Pandemic timing. Near-zero interest rates. Financing at conditions that will never exist again. They were disciplined, aggressive, leveraged at exactly the right moment. The market moved. They moved with it. Now they do it full-time. They're genuinely wealthy from it.

And I know a fund manager who oversees a billion-euro portfolio. He buys entire city blocks. He also recommends I get into real estate. Every time I see him. His deals come from contacts he's cultivated for a decade. He IS the dealflow. He doesn't look at listings. He gets called before listings exist.

Both of these are real. Neither of them is a model I can copy.

The couple got rich during a specific window: low rates, rising prices, positive cash flow from rents. That window opened around 2010 and closed somewhere around 2022. The people who entered late are now subsidizing their properties every month, waiting for appreciation to bail them out. That's not investing. That's speculation with a thirty-year time horizon.

The fund manager is a professional operation. A billion-euro fund. A decade of relationships. The ability to move fast, at scale, on off-market deals before anyone else can bid. That's not "buying an apartment to rent out." That's a different job.

Real estate investment has made people wealthy. Those people were either very well-timed or running a professional operation. Most people doing it today are neither.

But here's my real argument. Even if the numbers worked perfectly. The cash flow, the appreciation, the leverage ratio. I still wouldn't do it.

Not exponential.

I'm in the early stages of what I believe is the most significant technological and economic transition in a generation. The question I ask about every investment is: does this compound with the wave, or does it sit on the shore?

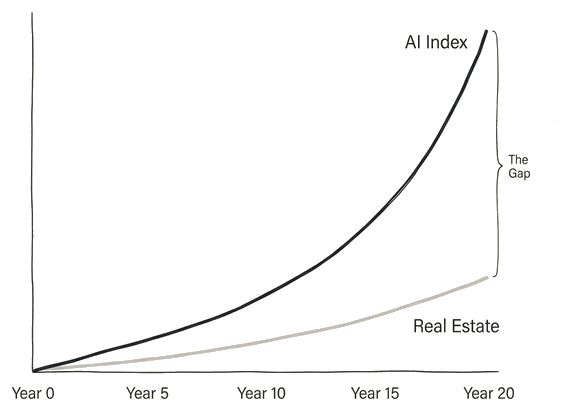

Real estate sits on the shore. At best it yields eight to ten percent annually on invested capital, in a good market, managed professionally. Semiconductor-focused indices have averaged ~18% per year over the past nineteen years. Fully liquid. Zero admin. No tenants. No refinancing.

The gap between those two numbers, compounded over a decade, is enormous.

The full breakdown — nineteen years, five asset classes, year by year, all in This Has Happened Before: The Numbers.

And this is the beginning of the wave. Not the middle. Not the end. The beginning.

I invested energy into building that strategy once. Now I let it run. I have nothing else to manage. No tenants. No refinancing appointments. No repair calls.

At that point the choice became obvious to me: I'm not going to tie an anchor to my leg at the start of the biggest wave I've ever seen.

Real estate is a hedge against the AI wave. It protects you. The house won't disappear because of AI.

But I don't want to be protected from the wave. I want to ride it.

There's one more risk nobody puts in the pitch deck: regulatory and political.

Real estate, especially rental real estate, is politically exposed in a way that almost no other asset class is.

In Germany, the Mietpreisbremse limits what you can charge and how fast you can raise rents. In 2021, 56% of Berlin voters approved a referendum to expropriate large housing companies. The constitutional court struck it down. This time. But 56% voted for it. That's a signal about where the political wind is blowing.

Governments under housing pressure will reach for the tools that are visible and tangible. Large apartment portfolios are visible. They are a political target in a way that a position in a semiconductor ETF is not.

Illiquid assets, capped upside, regulatory exposure, admin overhead. Against: liquid, exponential, zero management, globally diversified.

I think property values will continue to rise. I'm not making a bear case on real estate as an asset.

I'm making a priority case.

In an exponential era, the most dangerous allocation mistake is not choosing a bad asset. It's choosing a slow one. Every euro locked in a three-to-five percent gross asset is a euro not compounding in the infrastructure being built for the next twenty years.

Real estate is ballast. Sometimes ballast is what you need.

I need sails. All of them. Nothing held back.

Newsletter

Only when there is something worth saying. Unsubscribe anytime.

Not financial advice. Their call was right for them. This is mine.