Cathie Wood projects $1.4 trillion in data center spending over the next five years.

Blackstone has committed $25 billion to AI data center and energy infrastructure in one US state alone. Sovereign funds deployed an estimated $120 billion into AI infrastructure in 2025. The narrative is everywhere: AI needs power, therefore own the power. AI needs space, therefore own the space.

These investors are not wrong about the demand. The infrastructure is being built. The question is whether owning that infrastructure is the right position. Or whether the returns end up somewhere else in the stack.

I think they end up somewhere else.

Because predicting AI demand is easy. Everyone is doing it. The harder question, the one that actually determines returns, is where that demand has to flow.

When I was running an agency, I watched automation come in.

It didn't ask permission. It arrived in product updates. Campaigns that used to require expert judgment began running themselves. And there was nothing you could do about it. The only question was: are you on the right side of it?

That question shaped how I think about capital.

I went through every layer of the AI economy, asking where value actually concentrates.

Agents. Thousands of people can build one with the same tools. The best few will win. You can't know in advance which one.

Healthcare and every other industry. Enormous potential everywhere. But the same logic applies to all of them: AI optimizes processes, reduces costs, creates efficiency. When everything is optimized, what remains? Efficiency is table stakes, not a moat. And healthcare specifically: I have no edge there, no domain knowledge, and no confidence I could hold through a correction.

Energy. Real demand growth. Regulated commodity. Returns capped by policy, not determined by markets.

Data centers. Capital intensive, regional competition, linear margins. Infrastructure. The pipe.

And there's a structural problem with data centers that rarely shows up in investor decks. A railway built in 1850 lasted a hundred years. The fiber optic cables laid during the internet build-out will still be running in 2040. Data center hardware — the GPUs, the compute stacks — gets replaced every three to four years. You're not investing in infrastructure. You're investing in a recurring cost center that has to be rebuilt from scratch on a short cycle. The pipes need constant re-pouring.

I kept eliminating.

What remained: the compute layer everything runs on, and the software that orchestrates it.

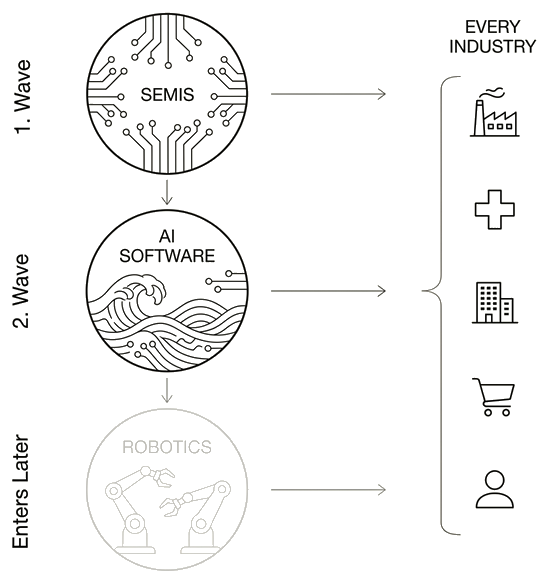

During the internet wave, bandwidth demand exploded. Server demand exploded. Physical infrastructure was being laid everywhere. But the companies that captured the returns were Amazon, Google, and the chip companies that powered them. Not the electricity providers. Not the operators of the server farms.

The economic rent didn't flow to the pipes. It flowed to what ran through them.

Same dynamic now. AI needs enormous power. The power companies are suppliers to the system. Not beneficiaries of the power law within it.

Here's the structural argument.

In exponential markets, value concentrates. The top node captures most of the returns. Everyone else shares what's left.

This happens at bottlenecks. The points everything has to flow through.

| Layer | Characteristics | Return Profile |

|---|---|---|

| Energy & Power | Commodity · Regulated · No scale effects | 4–8% p.a. |

| Data Centers | Capital intensive · Regional competition · Linear | Linear |

| Chips | Tokens per Watt · Power Law · Winner-take-most | ~18% p.a. (19-year historical) |

| AI Software & Platforms | Network effects · Zero marginal cost · Lock-in | Expected exponential |

| Applications & Agents | Many players · Low moats · Commoditizing fast | Uncertain |

The bottlenecks are chips and AI software. Everything else is capped by nature: by regulation, by capital cycles, by regional competition, by the fact that physical infrastructure is a linear input.

Only in these two layers does the exponential potential of AI actually compound without a ceiling.

If you invest across all layers, you dilute that. You average down from exponential into linear. The whole point is to not do that.

Of the two bottleneck layers, chips are the clearer bet right now. AI software is the right layer, but which platforms actually win is still open. AI-native companies are only beginning to generate proven use cases. The real money follows after the business model is proven, not before. That's why I hold the layer through an index, not individual names.

Two things make chips uniquely strong.

First: chips are needed throughout every phase of a GPT wave. Not just the infrastructure phase. As AI reshapes industries and eventually enters the physical world through robotics, every device, every robot, every model requires a chip. Demand doesn't peak. It extends.

Second: you don't need to predict which AI software platform wins. An index tracking the sector rebalances continuously, concentrating automatically into whoever captures the most value. You don't pick the winner. You own the mechanism that finds them.

Jensen Huang, CEO of Nvidia, was asked about the hardware shortage at a Morgan Stanley conference.

His answer: "Fantastic that everything is scarce."

Scarcity forces a decision. When data centers have limited power and space, they can't experiment. They can't afford an unproven vendor. They buy the most efficient option. Every time.

In AI infrastructure, efficiency means one thing: tokens per watt. How much intelligence from one unit of power.

Nvidia leads. By a lot. Scarcity makes operators even less likely to switch.

That's not a chip story. That's a power law story.

These are smart investors with access to the same data I have.

I don't think they're wrong about the demand. I think they're investing in the wrong layer of it.

There's also a structural difference in how I can hold. Institutional funds can't sustain a forty percent drawdown without losing clients. They have to go broader, more stable, more defensive. I don't. That asymmetry is part of the thesis.

I don't want to own the power grid. I don't want to own the building. I don't want to guess which healthcare company wins or which logistics firm optimizes best.

I want the layer that every winner in every industry has to run through.

That's not prediction. That's physics.

Newsletter

Only when there is something worth saying. Unsubscribe anytime.

Not financial advice. Your situation is different. Think for yourself.